Countries With the Highest National Debt: The Real Stories Behind Trillions That Shape the Global Economy

When we talk about debt, it’s easy to picture numbers on a screen — trillions here, billions there — but behind every statistic lies a country’s story. Debt isn’t just about overspending; it’s about choices, priorities, crises, and ambitions. Some of the world’s largest economies carry massive debts not because they are failing, but because they are financing the systems that hold the modern world together — from healthcare to highways, from education to innovation. Here’s a closer look at the countries that owe the most — and what those numbers really say about them.

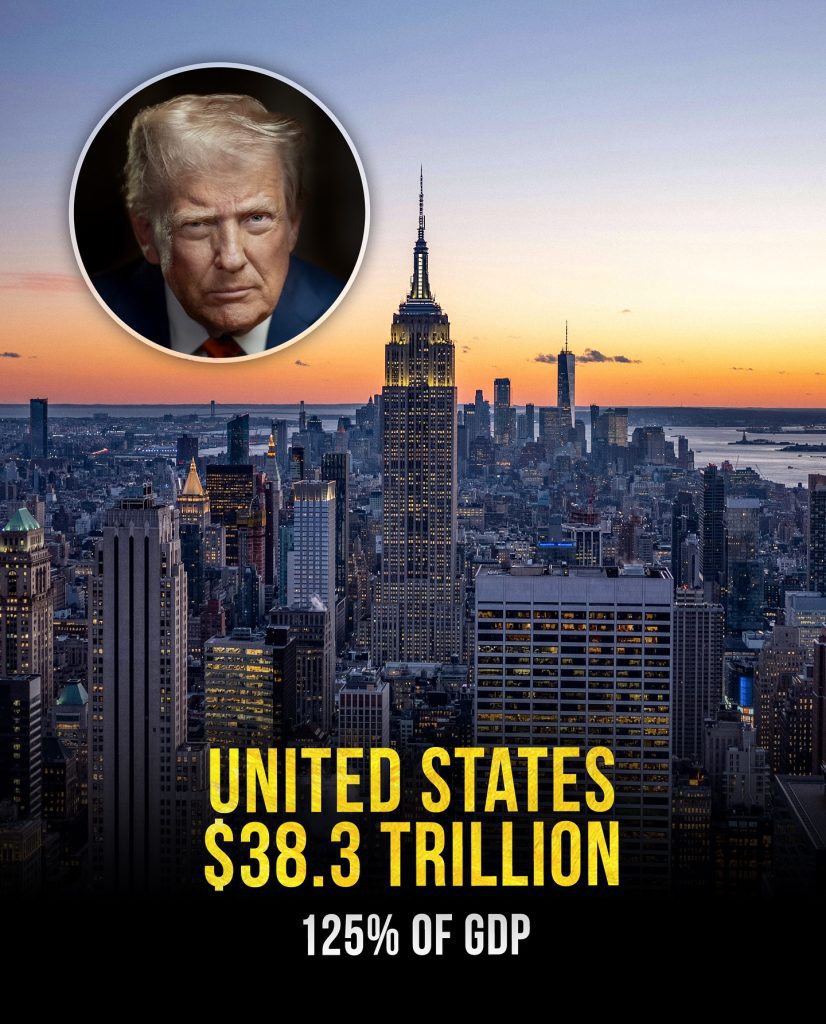

United States — $38.3 Trillion (125% of GDP)

The United States sits atop the list, holding the largest national debt in history — over $38 trillion, equal to about 125% of its GDP. For decades, America has relied on borrowing to fund everything from defense and infrastructure to social programs and economic stimulus. Every major crisis, from the 2008 recession to the COVID-19 pandemic, added another surge to the debt ceiling.

Despite the eye-popping figure, the U.S. remains one of the most trusted borrowers in the world. Investors continue to buy American Treasury bonds because of the country’s stability and influence. But even that trust has limits. Rising interest rates, political gridlock over spending, and growing entitlement costs are fueling concern that the U.S. could face difficult trade-offs in the future — higher taxes, reduced programs, or inflation pressure. For now, America’s strength still lies in the power of its economy and the global faith in its dollar.

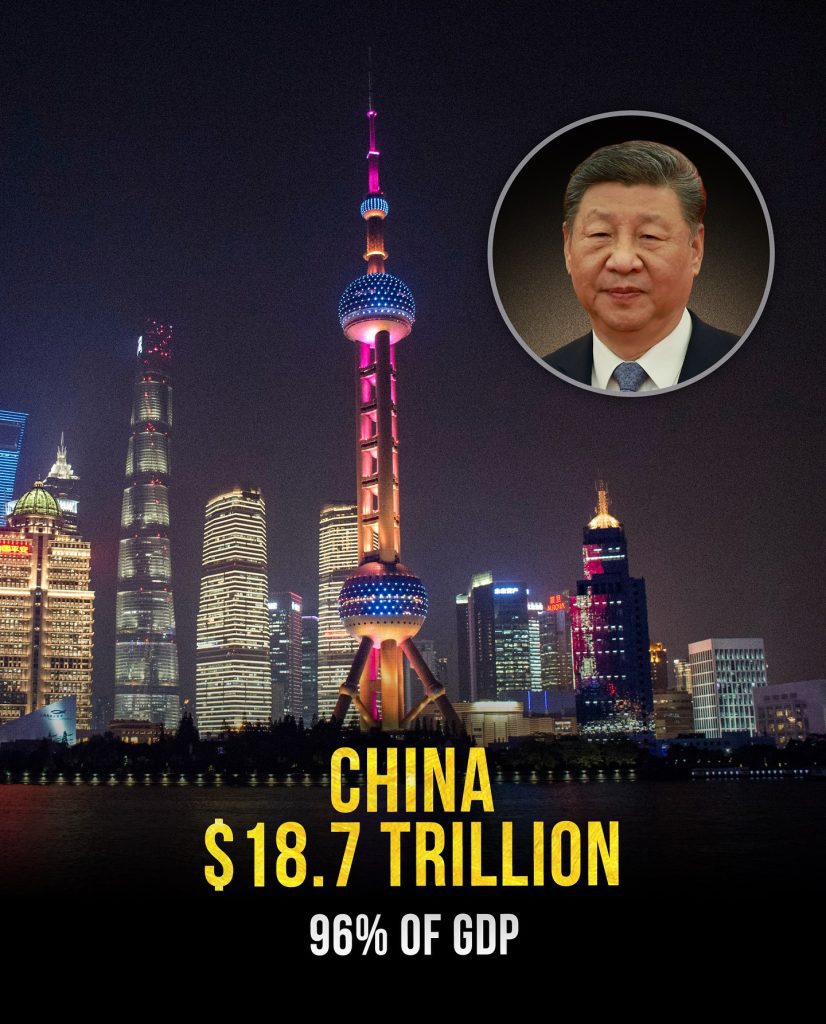

China — $18.7 Trillion (96% of GDP)

China’s national debt tells a story of rapid transformation. With about $18.7 trillion owed, Beijing’s borrowing has built cities, highways, railways, and industries that helped lift hundreds of millions out of poverty. But that same aggressive investment model has led to risks that now shadow its growth.

Local governments, real estate developers, and state-owned companies have borrowed heavily — sometimes too heavily — creating what economists call “hidden debt.” The country’s GDP-to-debt ratio remains under 100%, but cracks in the property market and slow recovery from the pandemic are testing China’s resilience. For President Xi Jinping’s government, managing this balance — keeping growth alive while avoiding a credit crisis — may define China’s economic path for the next decade.

Japan — $9.8 Trillion (230% of GDP)

Japan holds the world’s highest debt-to-GDP ratio at an astonishing 230%, yet it remains one of the most stable economies on Earth. This paradox has fascinated economists for years. After decades of low inflation and slow growth, Japan turned to borrowing to stimulate its economy and fund social welfare for its aging population.

The debt may sound alarming, but most of it is owed internally — to Japanese citizens and institutions — which makes it far less risky than it appears. The country’s ultra-low interest rates and disciplined financial management allow it to sustain such levels without panic. Japan’s story proves that context matters: debt isn’t just about numbers, but about who holds the bill and how it’s managed.

United Kingdom — $4.1 Trillion (103% of GDP)

The United Kingdom’s $4.1 trillion debt reflects years of balancing economic recovery, healthcare funding, and post-Brexit adjustments. The U.K.’s debt level now exceeds its total annual output, hovering around 103% of GDP — a milestone not seen since the aftermath of World War II.

Rising inflation and interest rates have added pressure on the British government to control spending while protecting households from cost-of-living struggles. Prime Minister Keir Starmer faces the challenge of maintaining public services without further deepening the debt burden. For the U.K., the goal isn’t eliminating debt overnight — it’s about restoring steady growth and rebuilding financial confidence after years of economic turbulence.

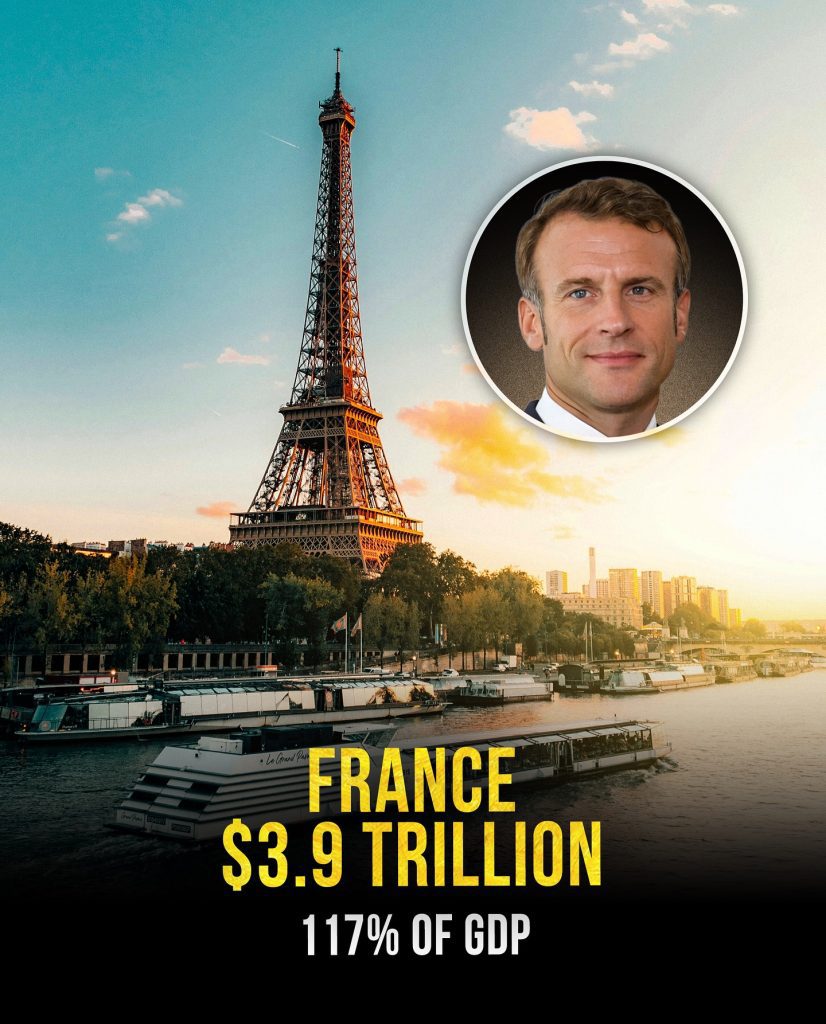

France — $3.9 Trillion (117% of GDP)

France carries a debt load of nearly $3.9 trillion, representing 117% of its GDP. Like many European countries, France’s borrowing increased sharply during the pandemic as the government supported workers, hospitals, and businesses. President Emmanuel Macron’s administration now faces the complex task of reducing debt without undermining public trust.

The French economy remains strong, but rising pension costs and labor strikes over economic reforms highlight the tension between fiscal responsibility and social welfare. France’s challenge is universal — finding a balance between progress and sustainability.

Italy — $3.5 Trillion (137% of GDP)

Italy’s $3.5 trillion national debt — roughly 137% of GDP — is one of Europe’s biggest economic worries. For decades, Italy has struggled with slow growth, political instability, and an aging population that strains its public finances.

Yet, Italy’s economy is far from broken. It’s a global hub for fashion, manufacturing, and tourism, with vast private wealth balancing much of its public debt. Prime Minister Giorgia Meloni faces a long road ahead in managing spending while keeping investor confidence alive. Italy’s story reminds us that debt is not just a problem — it’s a symptom of how nations choose to prioritize their futures.

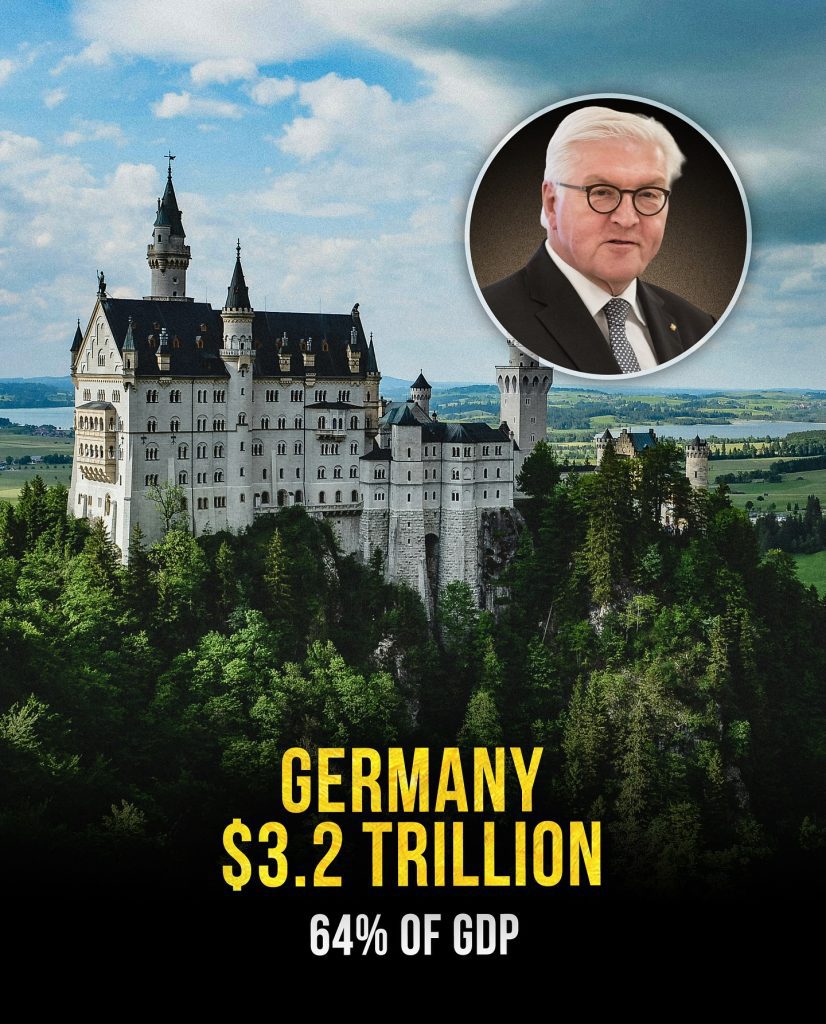

Germany — $3.2 Trillion (64% of GDP)

Germany stands out for its discipline. With $3.2 trillion in debt — just 64% of GDP — it remains one of the most fiscally conservative nations among major economies. Known for its “debt brake” rule, Germany limits how much it can borrow, focusing on balanced budgets and long-term stability.

However, even the strongest economies face pressure. Energy challenges following the war in Ukraine and the shift to green technology have forced Berlin to reconsider spending. As Europe’s industrial engine, Germany’s cautious approach shows that moderate debt can still coexist with growth when combined with strong export performance and disciplined policy.

Canada — $2.6 Trillion (114% of GDP)

Canada’s debt, about $2.6 trillion or 114% of GDP, reflects a mix of resilience and risk. The country managed the pandemic with heavy public support programs, which lifted its debt but also cushioned millions of citizens. As the Bank of Canada raised interest rates to combat inflation, servicing that debt became more expensive.

Canada’s strength lies in its natural resources, skilled workforce, and stable banking system, but like others, it must balance growth with caution. The government faces calls to rein in spending while maintaining its reputation as one of the world’s most trusted economies.

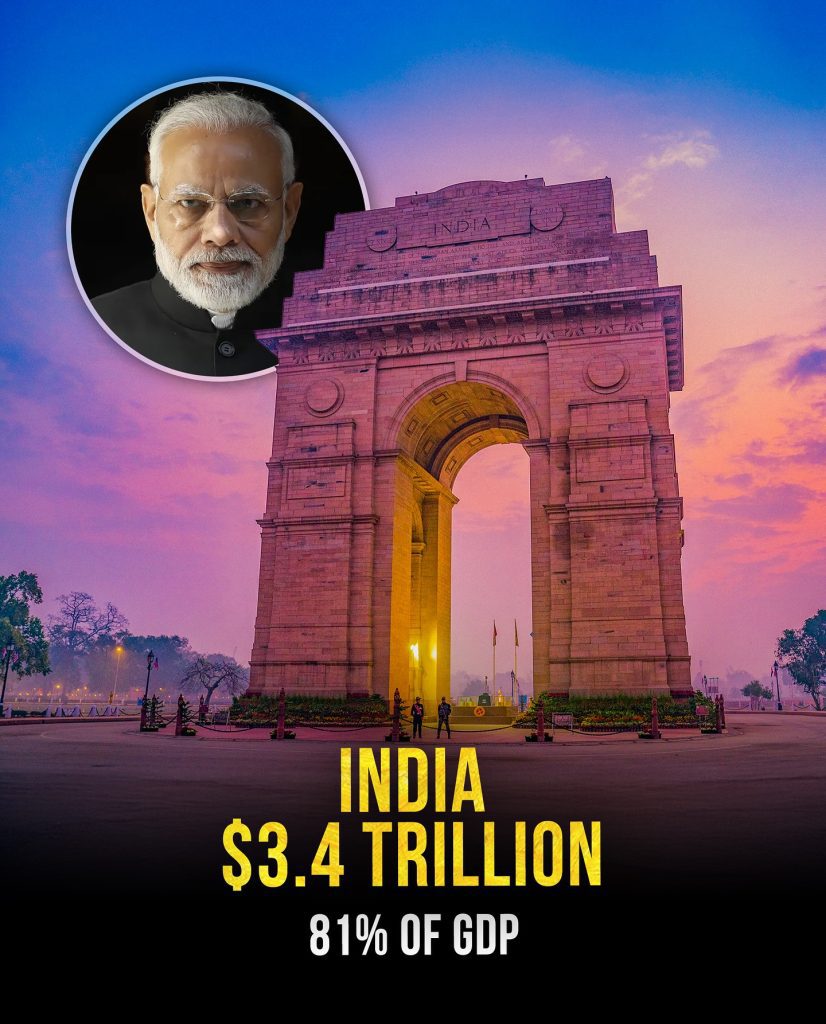

India — $3.4 Trillion (81% of GDP)

India’s $3.4 trillion debt may sound large, but it’s far more manageable than many developed nations’. At 81% of GDP, it reflects a developing economy investing heavily in its future — from highways and digital infrastructure to defense and education.

Under Prime Minister Narendra Modi, India has focused on rapid industrialization, foreign investment, and technology-led growth. Debt has played a crucial role in this transformation. While challenges like unemployment and inflation persist, India’s expanding economy and young population provide the momentum needed to sustain progress. In many ways, India’s debt is a bet on tomorrow.

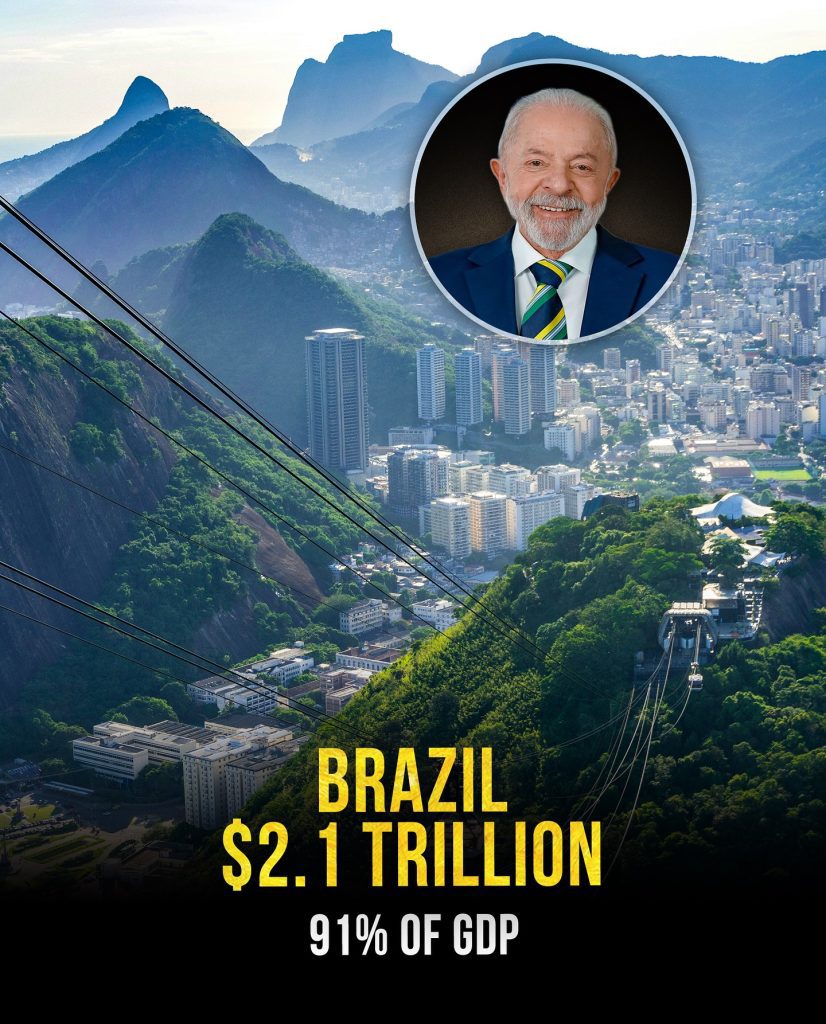

Brazil — $2.1 Trillion (91% of GDP)

Brazil’s $2.1 trillion debt, nearly 91% of GDP, captures the story of Latin America’s largest economy — dynamic, diverse, but often turbulent. Over the years, inflation, political uncertainty, and welfare spending have kept Brazil’s debt high.

President Luiz Inácio Lula da Silva’s administration is now trying to stabilize public finances while investing in social programs and environmental recovery. Despite economic volatility, Brazil’s agricultural and energy sectors continue to grow, keeping the country’s potential strong. Debt here reflects both a struggle and a promise — the price of balancing people’s needs with economic reform.

The Bigger Picture

National debt isn’t inherently good or bad — it’s a reflection of choices, crises, and ambitions. The United States borrows to maintain its global influence. Japan uses it to care for its elderly population. China uses it to build the infrastructure of the future. Each country’s approach reveals what it values most.

The real question isn’t how much a country owes, but how it uses what it borrows. Debt can be a burden or a tool — and history shows that the smartest nations find a way to turn it into opportunity.